Why Multifamily?

The Principals believe the current dynamics within the multifamily real estate market will create compelling opportunities for sophisticated investors with discretionary capital to invest. The Fund will selectively invest capital in specific multifamily properties and markets to capitalize upon the recent upheaval in, and subsequent recovery of, the underlying multifamily and capital and housing markets. The Principals believe the Fund offers a compelling investment opportunity due to the following factors:

Favorable Supply / Demand Fundamentals:

- Limited Construction Pipeline:

With current values below replacement cost, it is cheaper to buy than build, resulting in a significant decline in new construction. In addition, while debt is available today for the purchase of apartment properties, development capital is limited. As a result, the National Association of Home Builders projects 2011 multifamily housing starts of only 133,000 units, approximately 40% of the long-term average. Taking into account population growth and the obsolescence of aging properties, approximately 400,000 units per year are required to meet national housing demand, significantly higher than projected development in the near term.

Source: Integra Realty Resource – IRR-Viewpoint Report

- Echo “Boom”:

Overall rental demand is expected to grow rapidly over the next five years, supported by favorable trends among predominantly renter cohorts. Growth in population aged 18 to 34 – the group with the highest propensity to rent, or “prime renters” – is resuming after two decades of decline. By 2015, the echo boomer population aged 18-34 is projected to reach 66 million (nearly as large as the peak the baby boom) and won’t peak until 2020.

- Prime Renters Living at Home:

In 2009, 29.4% of adults 18-34 years old were living with their parents, well above the 27% – 28% range that prevailed during the past quarter-century. The total number of young adults living with parents is a record 20.3 million. If an economic recovery brings the share down to 27%-28%, it would significantly increase the number of households, most of whom would be renters.

- Economic Recovery:

Through the latter half of 2017, job creation among the prime renter age cohort of 20-34 year olds significantly outpaced the broader market. Rent and occupancy levels, which are directly correlated to job growth, are poised to benefit from the projected economic recovery over the near-to-mid term.

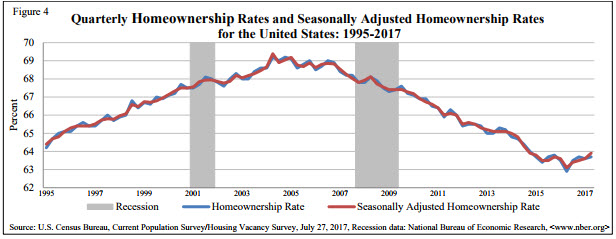

- Declining Homeownership:

Homeownership has begun to decline and is projected to continue to do so. The combination of more stringent mortgage underwriting standards and the wealth destruction of the recent cycle is increasing barriers to homeownership and pushing households into apartments. With approximately 114 million households in the U.S., every 1% decline is equal to 1.14 million units of additional rental demand.

Source: US Census

Source: US Census

Hedge Against Inflation:

In addition, apartments have shorter leases than other property types, allowing near-term realization of recovering market fundamentals and changing market conditions.

Low Volatility/Transparency:

- Less Volatility:

Apartments have historically experienced much lower variability with respect to market rents, vacancies, and valuations than other property types. In addition, multifamily assets have limited revenue concentration risk. Unlike other property types, where individual tenants can occupy a large portion of the asset, revenue decline from any one multifamily tenant vacating minimally impacts gross revenue. - Transparency:

Monthly leasing activity due to shorter lease terms results in continuously updated data points on market rents and concessions.

Efficient Attractive Financing:

Apartments have access to low cost and readily available debt financing from Government Sponsored Enterprises (GSEs), including Fannie Mae, Freddie Mac and the Federal Housing Administration. In addition, due to the transparency and low volatility mentioned above, insurance companies typically offer their most aggressive terms on multifamily assets.

- Use of Leverage: In addition to the proceeds from the Equity offering, the Fund will borrow additional monies to purchase and provide for capital improvements that will permit increased diversification and potential returns of the fund. The use of leverage will be carefully balanced to maximize investment returns while preserving a solid, safe economic foundation.

- Strong Current Yields: Due to low capital expenditures and tenant improvements relative to other property types, cash flow for apartments averages 83% of NOI; other property types range between 64% and 74%1.

Attractive Financial Returns:

Our Multifamily investments seek to achieve a rate of return in excess of typical alternative investment returns.

Tax Advantages:

Multifamily investments have higher after-tax yields due to a shorter depreciation schedule. For example, based on a 27.5-year depreciation schedule, a current after-tax yield of 10% would imply a pre-tax equivalent yield of approximately 15%2. Upon sale, profit over depreciated basis is mostly taxed at the capital gains rates, which are lower than ordinary tax rates.

Real Estate Ownership:

Investors receive all the benefits of real estate ownership with none of the management headaches.

- Appreciation

- Depreciation

- Loan Principal Paydown

Strong Financial Commitment from the Principals:

The Principals and their affiliates will offer preferred returns to investors and subordinate their returns to investors, directly and materially aligning their interests with those of the investors. The Principals also invest their own money into each deal alongside their investors. They practice the “if it’s not good enough for our money, it’s not good enough for our investors” approach to investments.

Experience and Track Record of the Principals:

The Principals combined have over 50 years of experience in business ownership, management, and real estate investments.

1″A Case for Investing in U.S. Apartments” – CBRE Torto Wheaton Research, March 2009

2 It is anticipated that depreciation expense (which is a non-cash deduction) may offset current taxable income such that the current distributions received will be equivalent to an after-tax yield. If one were to invest in an alternative investment that did not have depreciation expense shielding current taxable income, to achieve a similar after-tax yield of approximately 10%, assuming a 35% tax rate, the pre-tax yield would need to be approximately 15%.